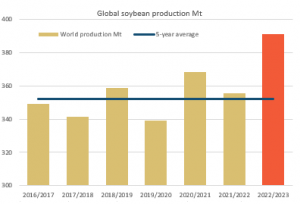

| In the USDA’s October WASDE report released today, global soybean ending stocks were revised up by 1.6Mt to 100.52Mt for 2022/2023. This puts global soybean ending stocks 8.14Mt higher than last year’s level and `1.17Mt higher than its 5-year average. Higher global ending stocks were mainly the result of a 1.6Mt increase in Brazilian ending stocks (31.31Mt for 2022/2023), while US ending stock estimates were unchanged from last month’s forecast and Argentina’s 2022/2023 ending stocks were revised lower. In terms of production, global soybean production was 1.22Mt higher to 390.99Mt in October relative to the USDA’s September forecast. Largely due to a 3Mt upward revision to Brazilian production for 2022/2023 to 152Mt.

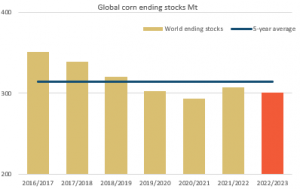

In terms of corn, global ending stocks are now projected at 301.19Mt, which is down 3.34Mt from last month’s estimate, down 5.83Mt from the previous year’s level and 12.51Mt below its 5-year average. Ending stocks in both the US and China were revised down. Global corn production was revised down by 3.84Mt to 1168.7Mt, mainly the result of weaker US and EU output for 2022/2023.

Looking at wheat, global ending stocks are seen reaching 267.54Mt for 2022/2023, which is down 1.03Mt from last month’s forecast, down 8.47Mt from last year’s levels and down a massive 17.85Mt from its 5-year average. Global wheat production was also revised lower by 2.22Mt to 781.7Mt in the October update compared to September. This puts wheat production 16.48Mt below its 5-year average and mainly reflects weaker output from the US, where 2022/2023 production was revised down from 48.5Mt in September to 44.9Mt in October.

For more analysis and opinions, see this week’s grain report. |